The Real Cost to Build a House. How to Get the Number in Under 10 Minutes

Most first-time builders think the number their builder quotes them is the cost to build.

It isn't. It's missing enough to run them out of money halfway through.

A napkin estimate can land $189,000 short of the cash a builder actually needs to start. Soft costs that nobody quotes can add ninety grand to a build. A single sloped lot can double a foundation before anyone touches a shovel.

Those builders aren't bad at math. They make the same mistake every time - pricing the house everyone talks about instead of the one they actually have to pay for.

This guide breaks the real number down line by line. Follow a few simple steps and you'll have it in under ten minutes - hard costs, soft costs, and the cash you need before the loan pays for anything. A free template does the math for you.

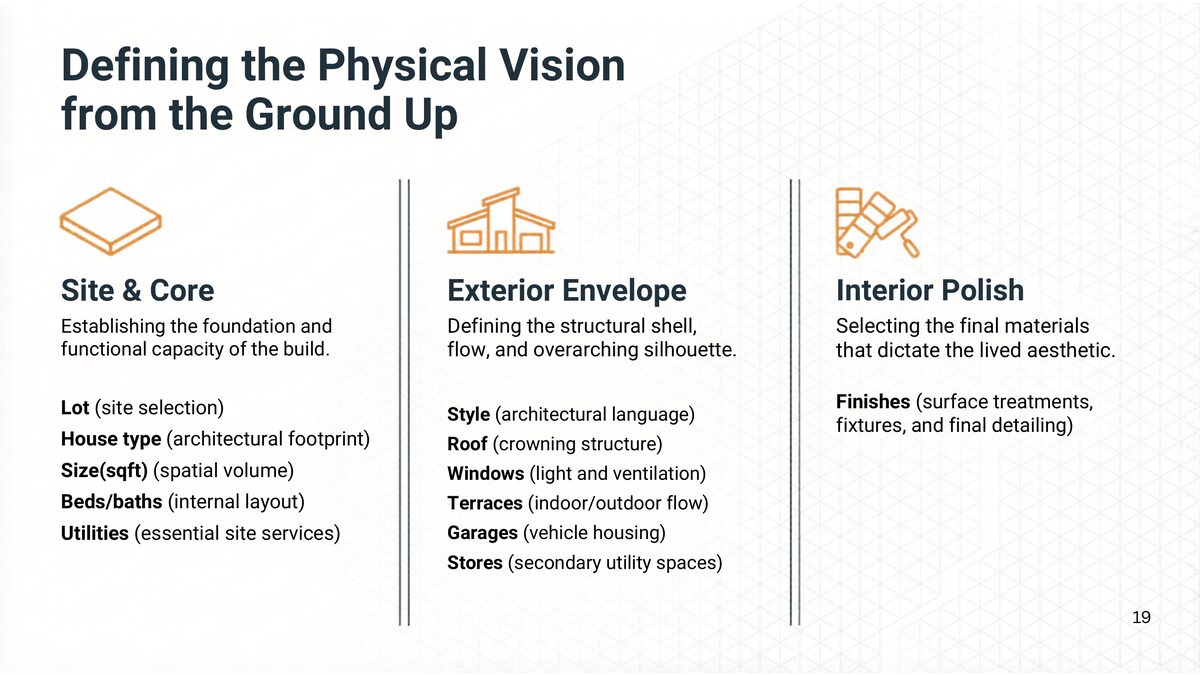

You can't put a price on a house you haven't defined yet

This is where almost everyone goes wrong on the very first move. They start Googling cost per square foot before they've decided what they're actually building.

Think about a car. If you ask me what a car costs, I can't answer you. A used commuter and a loaded SUV are sixty grand apart. A house is that same problem times a hundred.

So before any number, you define the physical vision. It fits on one page, and I break it into three buckets.

Fill those three buckets and you've turned "I want to build a house" into an actual spec. That's the only thing you can put a real price on.

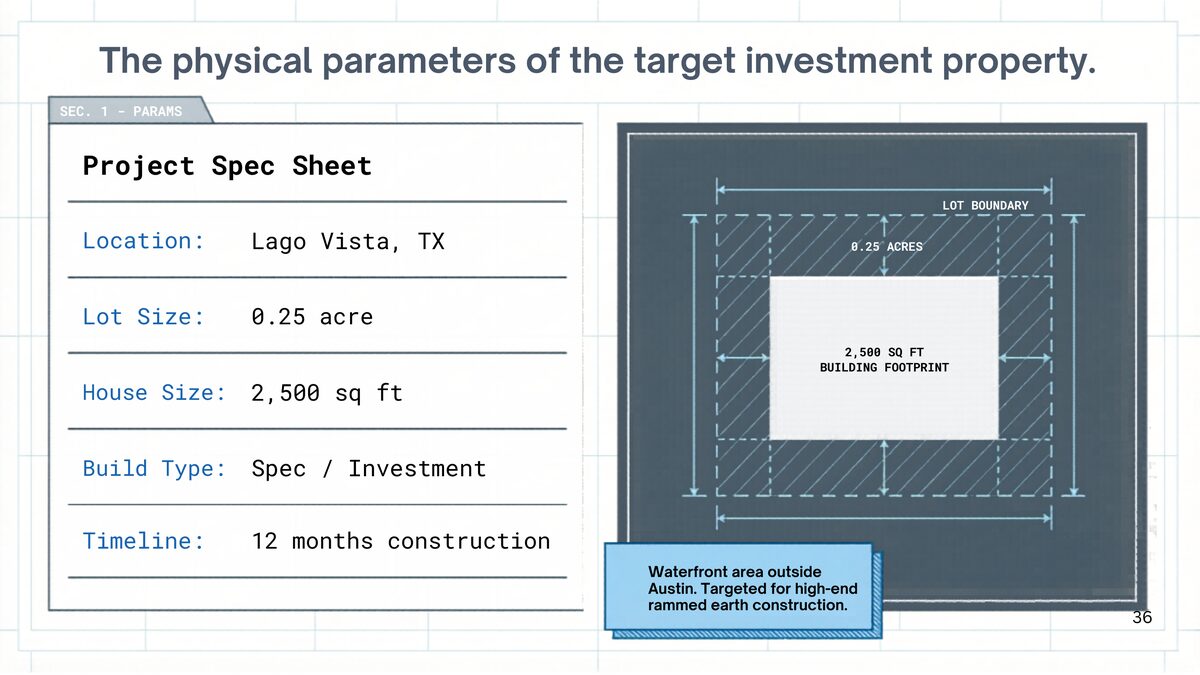

The house I'm using for the rest of this is a real one. A 2,500 square foot spec home in Lago Vista, just outside Austin. Not a $3 million showpiece - a normal house, the kind most first-timers actually build. I sat in on the numbers from the first napkin sketch to the final draw, so every figure below ties back to this exact build.

Question 1: What does it actually cost to build?

Now you can reach for the number everyone reaches for first - cost per square foot. Price per foot times your square footage. Done.

On this build that was about $220 a foot. Times 2,500 square feet, that's $550,000 to build.

Where do you get the per-foot number? Not a Google search - national averages are useless to you. The national average in 2026 ran around $160 a foot. If you want what's actually driving those 2026 numbers - materials, land, and labor - I broke it down separately. In Austin, for a build like this, you're closer to $220. The number is always local. You get it by finding homes going up in your area, in your style, at your size, and asking the builders nearby what they're running per foot right now. Three or four of those and you've got a real range.

Write it down. It's good enough to tell you if you're in the right universe before you spend another dime. But a number that clean hides everything that drives the cost. You don't know if it's high or low for your house until you crack it open.

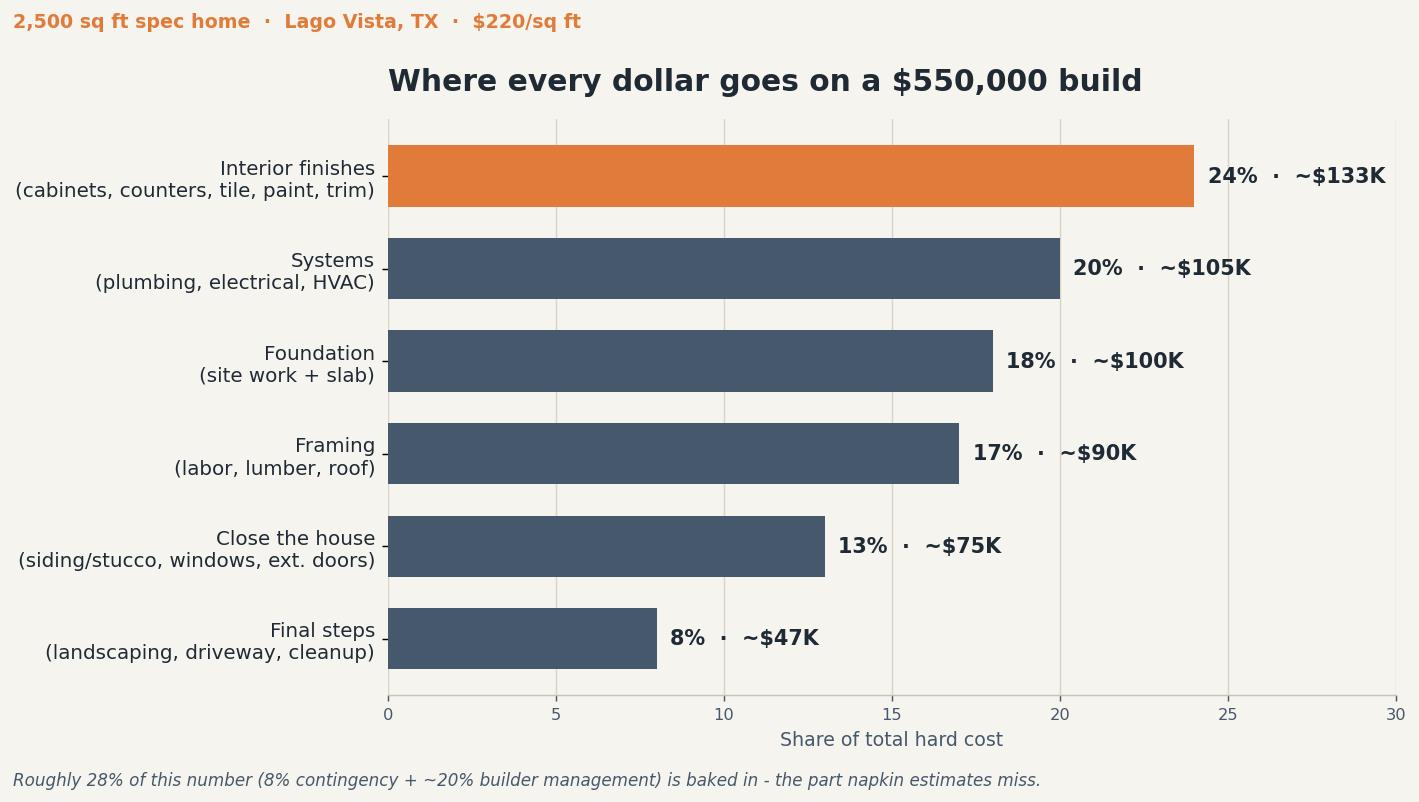

So here's the same $550,000, split the way the national builder data splits it. These shares hold up surprisingly well from one house to the next.

It starts in the ground. Site work and foundation - clearing, slab, footings, drainage. Around 18%, call it $100,000.

The frame goes up next, labor and lumber with the roof on top. About 17%, roughly $90,000.

Then you close the house - siding or stucco, windows, exterior doors. Around 13%, about $75,000.

Then the systems get run before they're covered - plumbing, electrical, heating, air. Bigger than people expect, close to 20%, about $105,000.

And here's the one that catches almost everyone. Interior finishes - flooring, cabinets, countertops, tile, paint, trim, fixtures. This is the single biggest chunk of your entire build. Not the framing. Not the foundation. The inside. Around 24%, roughly $133,000.

Then the final steps - landscaping, driveway, cleanup. The last 8 or 9%, call it $47,000.

Add it up and you're back to $550,000. Same number cost-per-foot gave you, but now you can see which rooms are quietly eating your budget.

And there's one more thing hiding inside that price. A builder always carries a contingency for surprises and a fee for managing the job. On this template, that's about 8% for contingency and 20% for management, baked right in. That's the real reason a back-of-the-napkin materials estimate always comes in low. You're leaving out the 28% that actually runs the project.

Question 2: The costs nobody is paid to warn you about

Even a perfect hard-cost number is missing an entire category of money. The one nobody quotes you, because technically it isn't the cost to build the house. Soft costs.

The reason first-timers miss them is simple - nobody is incentivized to bring them up. Your builder builds. Your lender quotes you a rate. Nobody hands you the full picture, because the full picture is your job, not theirs.

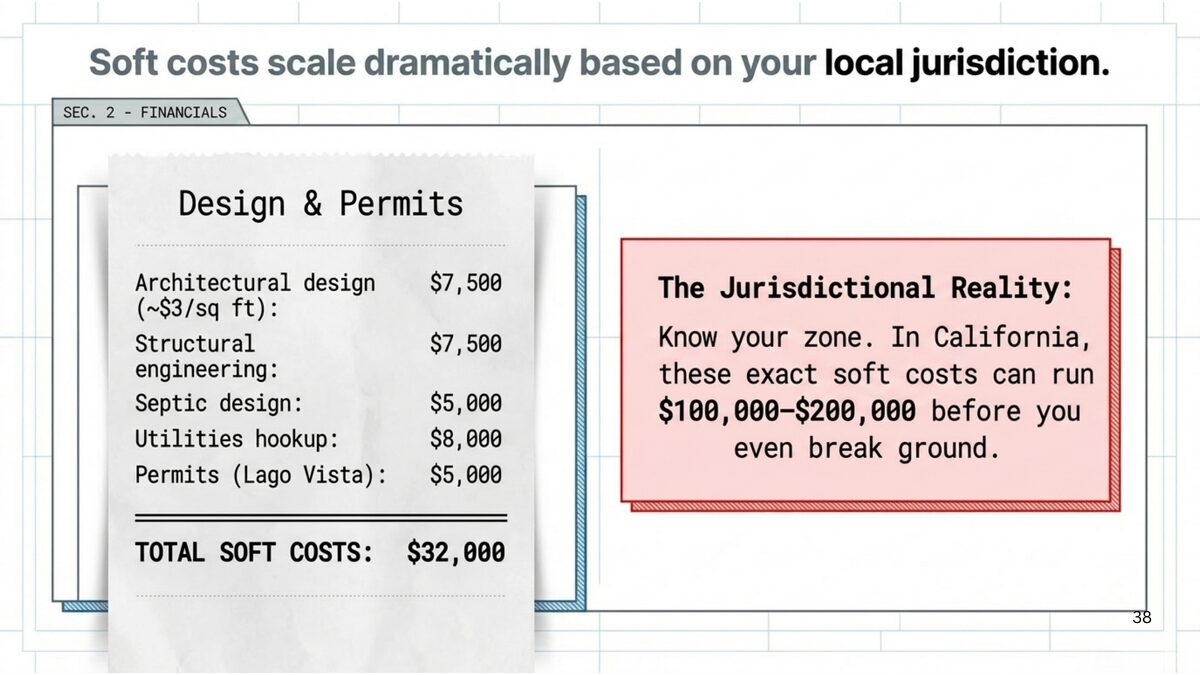

Here's what lived in the soft-cost bucket on this build.

Design and permits ran about $32,000 - architectural design, structural engineering, septic design, utility hookups, and the permit fees themselves. Loan points, the fee the bank charges just to open the loan, came to $11,000. Closing costs, another $6,000.

And the big one nobody budgets - interest while the house is being built. You pay interest every month on the money you've drawn, for the entire build. Twelve months of it on this one came to about $44,000. None of that is a brick or a window, but all of it comes out of your pocket.

Stack it up and soft costs cleared $90,000 before you even count the loan. Skip this bucket in your template and you can be that far short before you install a single door.

Question 3: Your lot can throw the whole number out the window

Everything so far assumes a normal lot. Flat, buildable, utilities at the street. Plenty of lots aren't, and the lot is the one place where a problem you can't see doubles a cost you didn't plan for.

A steep slope means more foundation, more engineering, more retaining walls. Bad soil means a more expensive foundation system. No sewer district means a septic system. Utilities far from the road means real money just to bring power and water in. None of that shows up in your perfect per-foot number, and none of it shows up in your line items until someone tells you it's there.

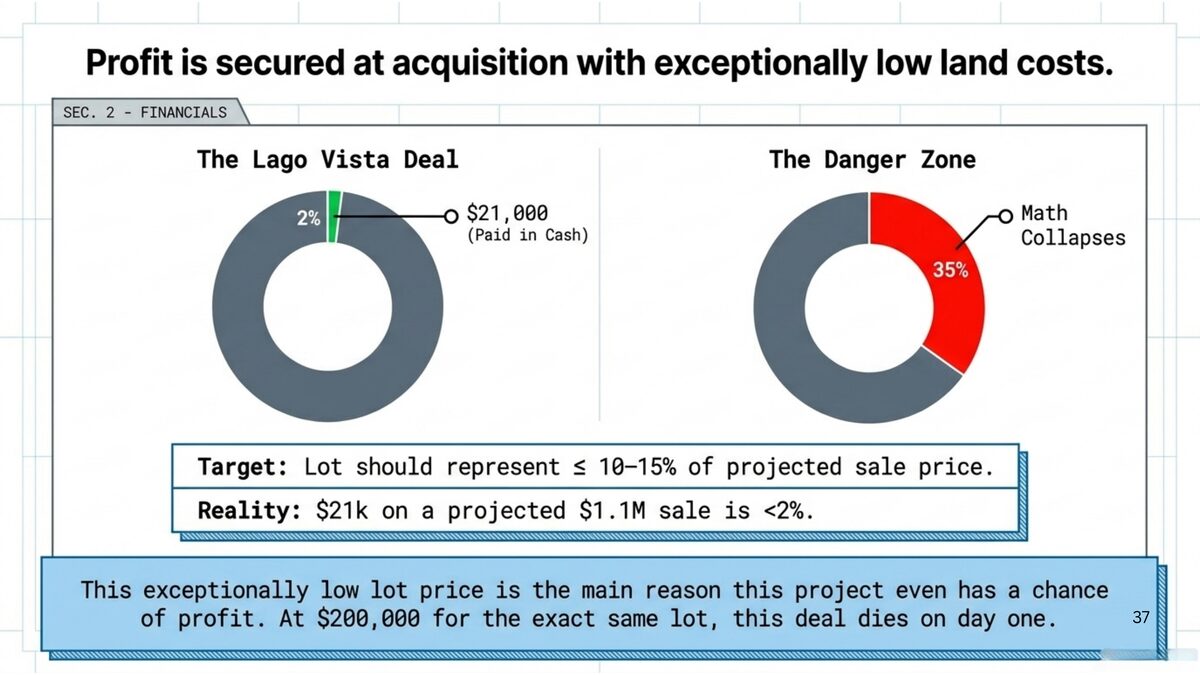

There's a rule on what you pay for the lot itself, too. On our build the lot was $21,000 against a projected $1.1 million sale - under 2% of the final value. That's exactly why this deal had room for a profit. The target is to keep your lot around 10 to 15% of projected sale price. Push past 25% and the math starts collapsing before you've even broken ground.

Before you make an offer on any lot, there are five numbers worth running first - I walk through them on a real Texas deal.

You can find all of this out the slow way - surveys, soil reports, a civil engineer. Or you can pressure-test the lot in a couple of minutes before you spend a dollar.

Question 4: The cash you need before the loan pays for anything

So now you've got the real cost to build - hard costs plus soft costs, on a lot you've actually checked. You'd think that's the whole picture. It isn't. There's one more number, and it's the one that actually stops builders from breaking ground.

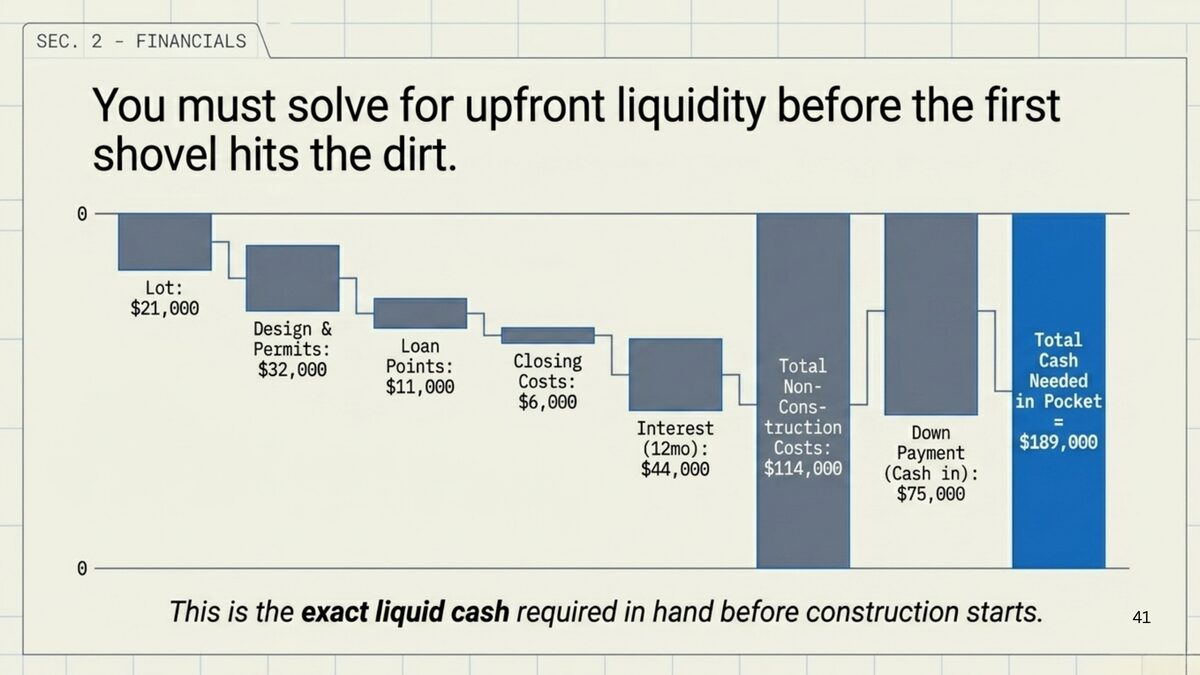

Your cost to build and the cash you need are two completely different numbers.

Most first-timers assume the construction loan just pays for everything. It doesn't work like that. A construction loan is a tab the bank runs. I made a seperate post to explain how it works - the system quietly rejects most first-time builders, and there are only a few real ways around it. They pay the builder in stages as the work gets done, then reimburse. Which means you fund the front of this yourself. You pay the cover charge before you ever get in the door.

Here's the real math on this house. The soft costs we just added up, around $90,000, plus the lot at $21,000, comes to $114,000 the loan does not hand you up front. Now add your down payment on the construction loan, call it $75,000, and you're looking at roughly $189,000 in cash in your pocket before a single shower hits the door.

That's the number nobody tells first-time builders. Not the cost to build. The cash to start.

This is also why one Austin builder I interviewed skipped the construction loan entirely and built with cash. When the cost of money alone runs into the tens of thousands, paying it to a bank starts to look optional.

The real number on one page

If you remember nothing else, remember how the number stacks up.

Start by defining the house - three buckets, one page - so you're pricing something real. Get your hard cost local, then break it open, because the interior finishes will be your biggest line, not the framing. Add the soft costs nobody quotes you, which cleared $90,000 here. Pressure-test the lot before you make an offer, because a bad one doubles costs you can't see. And separate your cost to build from your cash to start, because the loan won't fund the front - that was $189,000 in pocket on a $550,000 build.

The rough number your builder calls you with gets you close. Knowing what's inside it is what keeps you from running out of money in month seven.

Want the full system for budgeting and running your build? Our complete Building Your Home course covers every phase from land selection through final walkthrough, with the templates, coaching calls, and live on-site events in Austin.

Your turn: which number surprised you most when you priced out your build - the interest, the soft costs, or the cash you needed up front? Drop it in the comments. I read every one

Dmytro Bondar has spent 20+ years building educational companies, the last ten working with spec and custom home builders in Austin, Texas - on their projects, marketing, and production. He runs HouseBuilderPro, a YouTube channel and training program that teaches first-time and spec builders how to build a house from A to Z without losing money, with step-by-step guidance, coaching calls, and live on-site building events in Austin.

Questions about your specific project? Drop them in the comments - I respond to every one.