Why First-Time Builders Can't Get a Construction Loan (And the 4 Ways Out)

I still remember the look on Igor's face (my good friend and customer builder in Austin) after his 60+ lunch meetings in a row ended the same way.

He'd just moved to America. He had cash. He had a plan. And he had real skills - he'd built bigger projects back home in Europe than most of these lenders had ever financed. None of it mattered. No US credit history. No US build history. Nothing on paper that an American bank could check a box against.

So he kept taking meetings. Big banks. Private lenders. Hard money guys. Sixty million dollars of capital sitting across those tables, and every single one of them said a version of the same thing: "We like you. Come back after you've built something here."

He couldn't get the money to build. And he couldn't build without money.

If you've ever sat across from a loan officer and felt that exact wall go up, this post is for you. I'm going to show you why the trap exists, and the four ways first-time builders actually break out of it. Igor used one of them. I've walked clients through all four.

(I also walked through this whole thing on camera, if you'd rather hear it than read it - watch the full breakdown here. Otherwise, keep reading.)

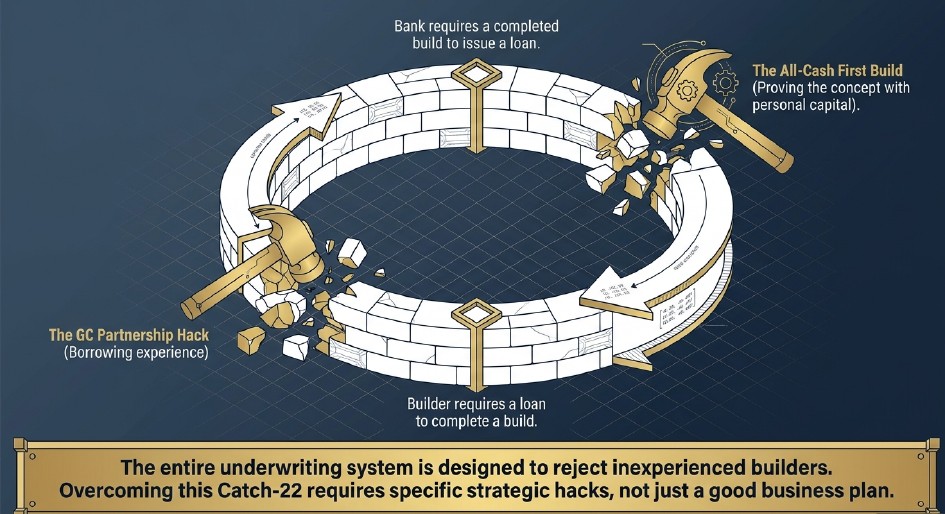

The bank isn't judging you. It's judging a building that doesn't exist yet.

Here's the thing almost nobody explains before you walk in.

When you ask for a construction loan, you're asking the bank to fund an asset that does not exist. There's no house. No collateral. No proof. All they have is you and a stack of drawings.

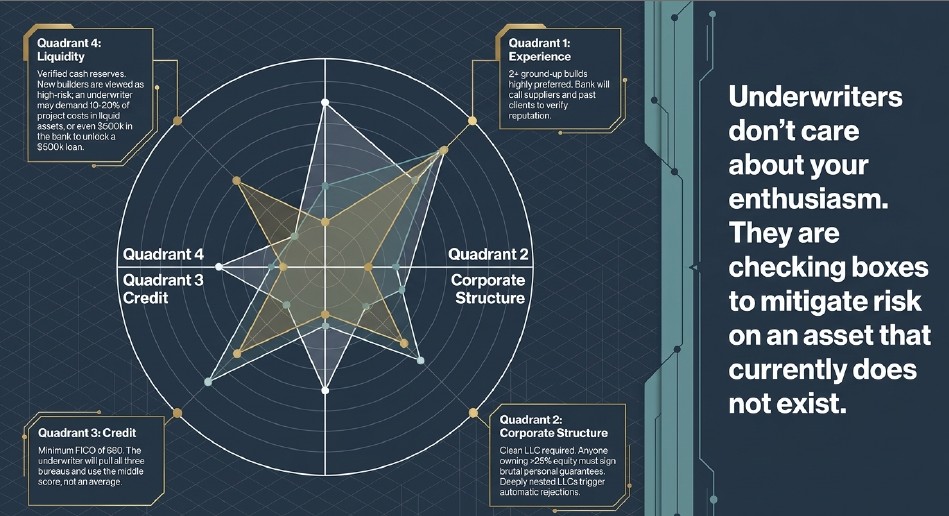

So they protect themselves the only way they know how - by checking boxes. I know exactly which boxes because I talk directly with construction loan managers, and this is what they want to see:

Two or more completed ground-up builds in the last few years

A minimum 680 credit score (they pull all three bureaus and use the middle score, not the average)

A clean LLC

10 to 20% of total project cost, verified and sitting in your business account

Read that list again as a first-timer. You can't check the first box without already having done the thing the loan is supposed to help you do. That's the trap. It's not personal. It's structural. The system is literally designed to reject inexperienced builders.

And the numbers back that up.

The data nobody hands you at the bank

New businesses under one year old face an 80-90% denial rate at traditional banks. (SBA / Federal Reserve survey data)

Construction is formally classified as a high-risk lending category, right next to restaurants and retail - thin margins, irregular cash flow, high failure rates.

About 48% of all loan applicants were denied on at least one application in the past year, and rejection rates are still climbing above pre-2020 levels. (Bankrate Credit Denials Survey)

Translation: a brand-new builder LLC walking into a big bank cold is fighting the worst odds in the entire lending market.

So the way out isn't to argue with the bank. It's to give them a different set of boxes to check, or to skip them entirely. Here are the four ways real builders do it.

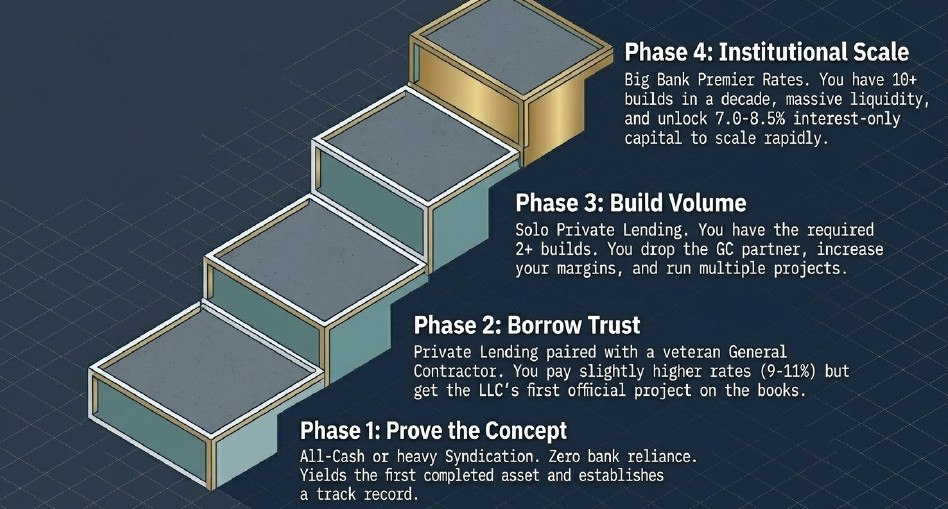

Option 1: Pay cash for your first build (brutal, but the cleanest)

This is the one Igor used.

You drain everything you have into one project. No leverage. No safety net. It's brutal, and it's not for everyone. You need real liquidity and you need to be willing to slow down for a year or two while you finish project number one.

But it works for one reason: once you've completed and sold that build, you have a paper trail. You've proven to the next lender that you can deliver and you can sell.

Remember how Igor's story ended? He paid cash, built his first house out of pocket, and during the open house for that finished home, a private lender walked in, looked around, and said: "We're ready to give you your first loan."

That's not luck. That's what a completed build does to the conversation.

One rule if you go this route: do it small. Don't burn your reserves on a $1 million custom home for your first one. Build something modest you can sell fast, and learn from it.

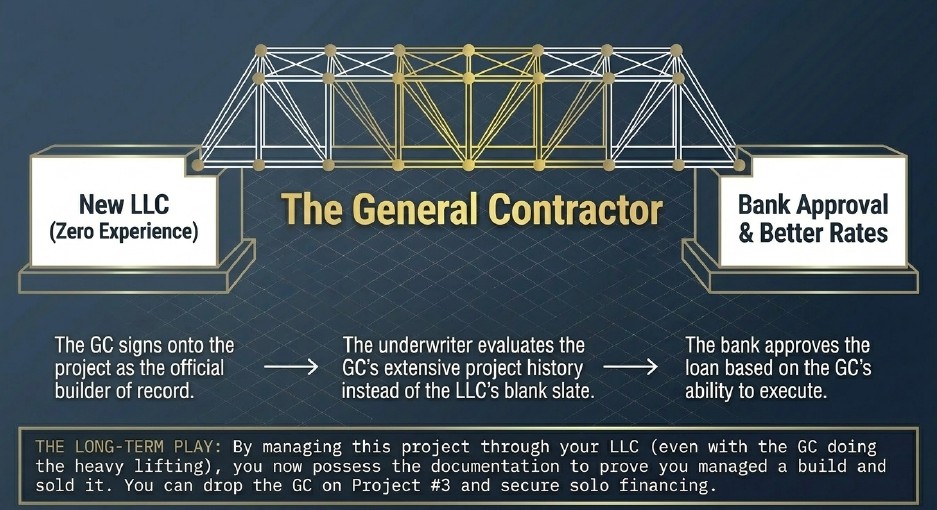

Option 2: The GC partnership (the move most first-timers have never heard of)

This is the most powerful option on the list, and almost nobody talks about it.

You set up your own LLC. But for your first project, you bring on a veteran general contractor - someone with a long track record - and you add them to the deal as the official builder of record.

The loan still goes through your LLC. But when the underwriter evaluates the application, they're looking at the GC's history, not your blank slate. You're not borrowing money. You're borrowing trust.

Here's the part most builders miss, and it's the whole game:

While the GC does the heavy lifting on the build, your LLC still owns the project, manages its own paper, and ultimately sells it. So when project number two comes around, the experience is on your record. You managed a build. You sold it. By project number three, you drop the GC, take the full margin, and walk into the bank as a real builder with real history.

I told a client recently - let's call him Raj, out of Dallas - exactly this. He wanted to come straight out of the gate with a $1 million custom build. I told him the truth: the bank will reject you on day one, no matter how good your numbers look. So instead, we go find a GC willing to attach their name and reputation in exchange for a fee or a piece of the upside.

The hard part isn't finding a GC. It's finding one willing to actually co-sign on the LLC with you, put their personal guarantee on the line, and bring the real build experience banks want to see. That's a lot to ask of anyone. It takes serious trust on both sides. Honestly, it's like a marriage - get the legal structure tied up tight, and pick someone you already have a strong working relationship with.

Option 3: Run a fix-and-flip first (experience without the ground-up risk)

If you don't have the cash for an all-cash new build but you do have enough to put down on a distressed property, this is my recommendation.

You set up your LLC, buy a distressed property, renovate it, and sell it. The bank sees that on your LLC's record as a completed real estate project. It's not ground-up, but most lenders count it as relevant experience when you eventually apply for a construction loan.

And here's why it actually trains you: you're learning the operational side for real. Managing subs. Hitting deadlines. Dealing with inspectors. Everything you'll do on a scratch build, just without the risk profile of pouring a foundation on day one.

Do two or three flips under your LLC and you walk into private lenders with a real story. Some will start treating you almost like a regular builder. I ran this exact path by a loan manager with deep experience here in Austin, and she confirmed it works.

Option 4: The cheap build (the ego killer that actually wins)

This is the one I lean on hardest with first-time clients, and it's the one most people resist.

Instead of starting with the dream project - the million-dollar custom home, the luxury spec on the hillside - you build something small. $200,000, maybe $250,000. Modest spec home, modest neighborhood. You build it as fast and lean as you can. And you sell it.

Now here's the part that's hard for builders to hear: making money on the first project is not the goal. Breakeven is fine. Even a small loss can be worth it. The goal is to walk away with a completed ground-up build under your name and a project history banks recognize and trust. That single completed project changes every conversation you'll ever have with a lender.

This was option four on the list I sent Raj. I asked him: what if, instead of starting with a $1 million commitment against a system built to reject you, you spent 6 to 9 months on a small build at a lower margin - and walked into your real project with experience, a list of contractors, and a reputation private lenders respect?

Most first-timers won't do this. Their ego wants the big project. But the ones who do almost always come out ahead.

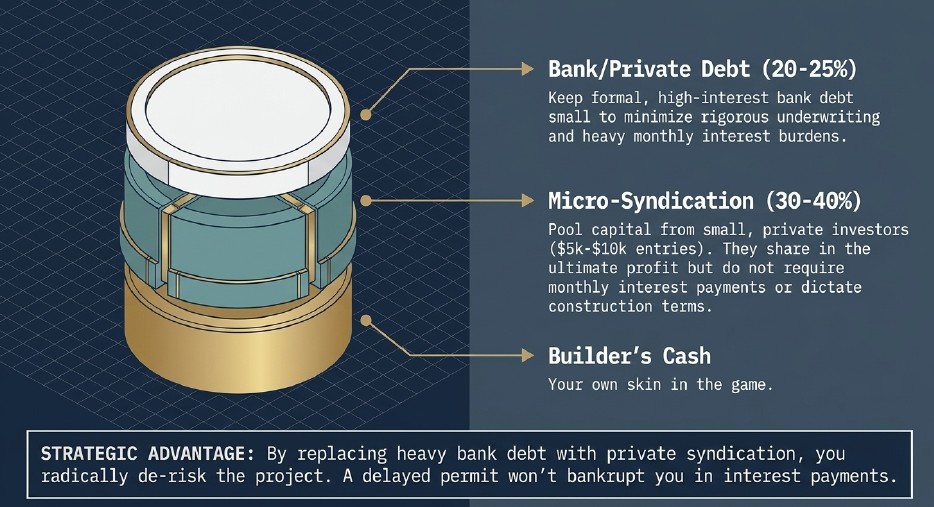

Bonus: You can skip the bank entirely

Not everyone wants to play the long game. So here's a fifth door.

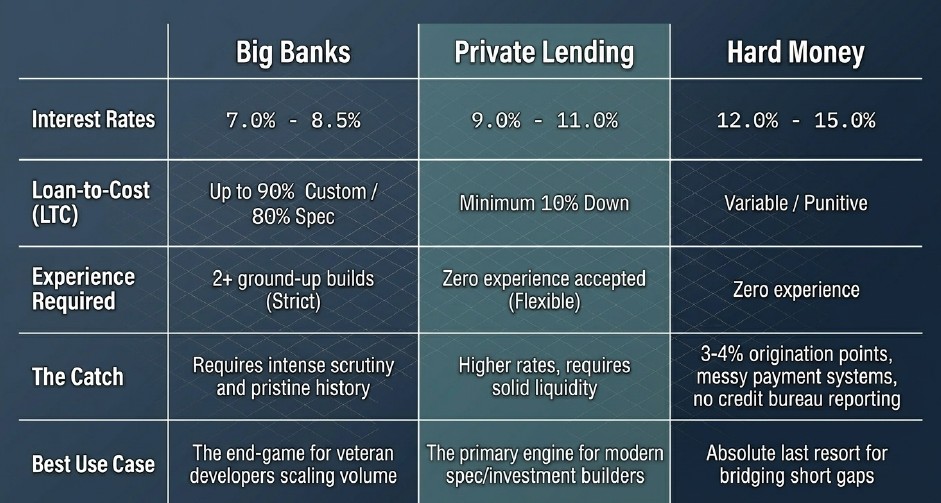

You can go around the bank completely with private lending. The rates are higher - think 9 to 12% instead of 7 to 8% - and they want to see solid liquidity. But many of them accept zero experience. For a lot of first-timers, that's the real starting point. Not Wells Fargo or Bank of America. A private lender.

The other option worth knowing about is micro-syndication. You pool capital from small private investors - $5,000, $10,000, $100,000 entries - and they share in the profit of the build instead of charging you monthly interest. No bank breathing down your neck. If permits take 18 months, you don't have monthly debt payments eating your margin while you wait on the city.

This is how a lot of working builders actually fund projects today. Bank debt is a small slice, maybe 20-25%. Micro-syndication covers another 30-40%. The builder's own cash covers the rest. The bank is one tool in the toolkit, not the only door.

The real lesson

The banking system isn't going to change to accommodate first-time builders. That door stays shut. But there are four ways through it - cash, the GC partnership, the flip-to-build, the cheap build - and one way around it entirely with private lending and syndication.

Igor didn't get lucky at that open house. He just finished the one build that turned every future "no" into a "yes."

So here's my question for you: which of these four doors is realistic for your next project - and what's the one thing stopping you from walking through it this year? Drop it in the comments. I read every one.

If you want the full version with Igor's story and all four plays walked through out loud, here's the video I made on this.

Before you go - two free things to get you funded

If you made it this far, you're serious about building. So here's what I put together for you.

1. The Construction Loan Readiness Check and Detailed video + list of banks. It's a short questionnaire that tells you, honestly, whether you're actually ready to get approved by a bank - or whether you should be running one of the four plays above first. Takes a few minutes. Download it here

Got a question about your specific situation? Drop it in the comments or email me directly. I read everything, and I'll see you in the next one.

Dmytro Bondar has spent 20+ years building educational companies, the last ten working with spec and custom home builders in Austin, Texas - on their projects, marketing, and production. He runs HouseBuilderPro, a YouTube channel and training program that teaches first-time and spec builders how to build a house from A to Z without losing money, with step-by-step guidance, coaching calls, and live on-site building events in Austin.

Questions about your specific project? Drop them in the comments - I respond to every one.

Want the full system for managing your build? Our complete Building Your Home course covers every phase from land selection through final walkthrough.